About the Book

India believed it could take development closer to its people, make the government more accountable, and empower women and oppressed communities through decentralisation—the provision of political and financial autonomy at the local level through the three-tier Panchayati Raj structure.

Fifteen years after the 73rd and 74th Amendments that brought in this innovation, what is the performance of the local government in India? Decentralisation, Governance and Development provides a comprehensive assessment that answers this question.

Drawing from the examples of the two states where decentralisation has been most successful—Kerala and West Bengal—this volume explores the causes and effects of failures in implementation and issues of governance. These essays by scholars from diverse disciplines, as well as policymakers and practitioners, will equip readers with both a theoretical understanding of the issues concerning local government, and the practical problems of designing and implementing policy framework in the field.

This book will be useful to students and scholars of development studies, economics, political science and sociology, and public servants and policymakers.

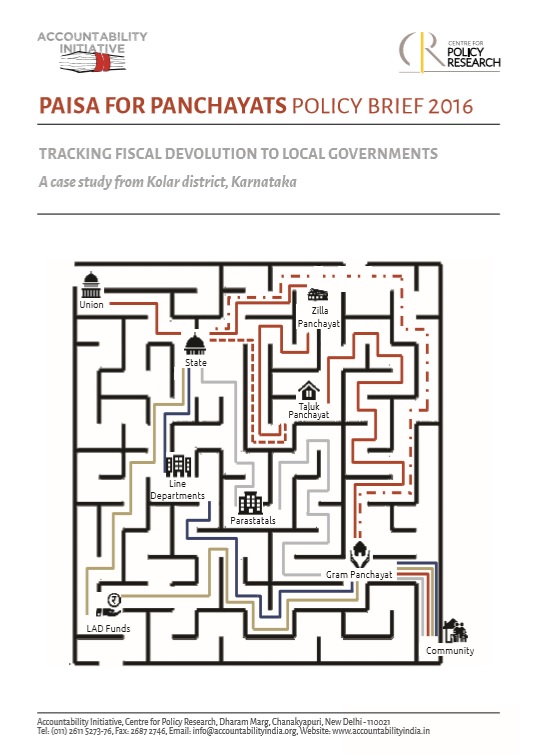

The study assesses the status of devolution of civic functions, role of parastatals in service delivery, structure of the transfer from state to Panchayats.

In 1992, the Government of India passed the 73rdand 74th amendments to adopt a decentralised model of governance.The Panchayat Briefs series examines the impact of these reforms in the context of new research on decentralisation in India. The second in this series examines the state of administrative decentralisation in India and the extent to which states have devolved the 3F’s (functions, funds and functionaries) to Panchayats