During the course of the PAISA survey our field level researchers gained some interesting insights regarding the ground level implementation of SSA. Their findings, trace different elements of the implementation story and include an analysis of the pattern of SSA fund flows, the status of school outputs and the level of SMC functioning. Here are some highlights from the field.

The curious case of missing uniforms

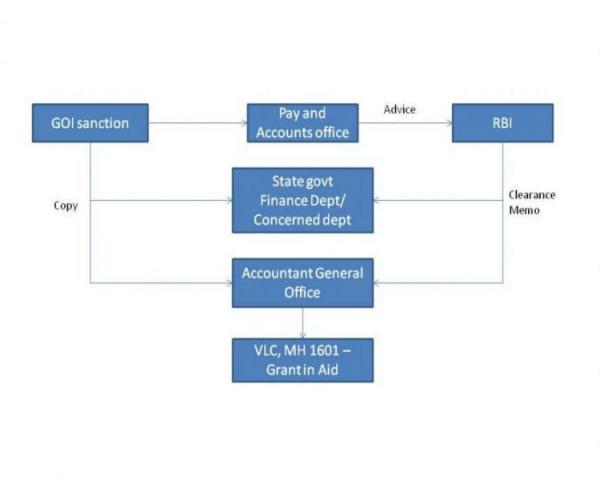

In this story Venugopal Kalokota, PAISA Associate, Andhra Pradesh, narrates a perplexing tale of the pattern of fund flows in Andhra Pradesh. In tracing the story, he demonstrates how confusion within the administration created delays in the provision of uniforms- a fundamental right of children under RTE.

Following the passage of the Right to Education 2010, the State Implementing Society (SIS) for Sarva Shiska Abhiyan, took a decision to provide two sets of uniforms to every student enrolled in a government elementary school. Funds for the uniforms were to be transferred to schools, who in turn where given the responsibility for purchasing uniforms at the local level. Consequently funds were transferred into school accounts in FY 2011(at a unit cost of Rs. 200 per uniform).

During the course of the PAISA survey, while scrutinizing the school passbooks, we found that although schools had received the uniform grant, none had spent it and in fact the funds had been re-appropriated back in to the district account. This seemed decidedly odd. On probing we learnt that later that year contrary instructions had been issued by the SIS to retrieve the grant amount transferred to schools! This was because the SIS, upon transferring money to schools, changed its mind and decided instead to procure uniforms centrally. To do this, the SIS office entered in to a contract with the Andhra Pradesh State Handloom Weavers Cooperative Society (APSHWCS). As a consequence of this administrative confusion, funds, once they reached the schools were ‘re-transferred’ to the state. The ultimate price however was borne by the students who did not receive their uniforms on time.

Status of School Outputs

One of the principal rights guaranteed under the Right to Education (RTE) is basic school level infrastructure. For Poonam Choudhary, PAISA Associate, Rajasthan it is the limitations in the provision of this right that have struck her the most. Based on her field level experience she paints a vivid picture of the status of infrastructure facilities and reflects on the question of who is responsible for the status of such facilities.

I have only ever known a school with all the necessary infrastructure facilities: boundary walls, playground, drinking water facilities, toilets and sufficient classrooms. During the course of the PAISA pilot survey, I found myself questioning this perspective. While conducting the pilot exercise in Chaksu Block I came across two schools whose story left a deep impression on me. In both schools the status of infrastructure facilities was extremely poor. One school was located on the main road but didn’t have a boundary wall. According to teachers the absence of such facilities made it extremely difficult to secure the school premises and equipment. In fact there have been occasions where the school building was used as a casino by local men who gambled there. One morning teachers and students arrived at school to find it strewn with liquor bottles and cigarette butts. Another time, a dead body was kept in the building due to lack of space. The school building it seems was the only building large enough to store the body!

The second school was located literally in the backyard of a house. The school lacked all the basic facilities. An asbestos shed served as a makeshift classroom. The only piece of furniture that the school had was a table for the head master. All school related material was kept in the granary. Piles of teaching-learning equipment and student registers were stacked near bags of wheat. There were no toilet facilities and the only drinking water facility was a hand pump that belonged to the family in whose house the school was located. Despite several applications sent by one of the only two teachers who taught in the school, the administration had not done anything to relocate the school and provide it with the necessary infrastructure facilities.

The combination of these two experiences raised questions in my mind. It provoked me to question whether it really made a difference that students were not getting what they should from our government. If yes, then who is accountable? In my view policy makers, government officials, teachers, students and the community are all accountable.

Teacher Absenteeism and Community Action

This story by Dinesh Kumar, PAISA Associate, Bihar documents the problems associated with the practice of officially sanctioned teacher absenteeism. Dinesh’s story also highlights the importance of community mobilization and the critical role that an active citizenry can play in demanding accountability from government officials.

My story relates to the school management committee of a government girls’ upper primary school, Karzahar village in Rohtas district, Bihar. This incident took place during the State assembly elections. Teachers were placed on election duty and as a consequence, schools across the state were operating below their full strength. In Karzahar village, out of the six teachers appointed, four were sent on election duty. As a result, children were attending school only to record their attendance! Concerned with the low level of teacher attendance, the Village Education Committee (VEC)(or School Management Committee as they are now referred to) complained to the Block Education Office (BEO) and filed an application requesting them to close the school for the period of the elections, since there were no teachers, what was the point of sending children to school – part from keeping attendance numbers high? The complaint lodged by the VEC, however, was summarily ignored and the school continued to operate.

I was made aware of this problem during an interview with the chairman of a VEC. The chairman explained that despite several attempts, the BEO had rejected their requests. The problem, it was later discovered, was that the BEO lacked the authority to respond to their requests, as it was the Block Development Officer who was responsible for assigning teachers on election duty.

Confronted with the problem, I decided, as a first step, to call for a meeting of the VEC. At this meeting it was decided that until such time that teachers did not return from election duty, all the literate members of the village would contribute their time and teach in schools. In addition we decided to explore alternate means to pressurize the local administration.

Following the meeting, a rally was launched at the Block Office. During the rally, the participants, particularly the children cornered the Block Education Officer and refused to let him leave until he promised to meet their demands. Hearing the ruckus, the Block Development Officer came out of his office only to be surrounded by the students who refused to listen to his platitudes. In the end, faced with enormous amount of pressure from the students and the community, the BDO finally relented and agreed to call back all the teachers who had been sent for election duty. The highlight of this story was that one of most active students in the protest was also the BDO’s daughter.

Lessons from a Participatory Planning Exercise

In her story of Sehore, Swapna Ramtake, PAISA Associate, Madhya Pradesh, highlights some of the most important lessons relating to the capacity of School Management Committees to plan and spend their resources. In her final analysis, she emphasizes the importance of both community participation and administrative support as critical elements for strengthening school level planning.

This story is about a school in Palaspani village, Narsulganj block in Sehore district where we conducted some preliminary work on strengthening the capacity of school based committees to make plans for meeting their needs.

When we first visited the village we did not have an inkling of the task that was before us. We were under the impression that once members of the school based committee (Village Education Committee) were identified, it would be a relatively simple affair to conduct a participatory planning exercise for the development of a school plan. How naive we were. In truth the greatest challenge was to motivate members of the community on the importance of education and their involvement in ensuring its delivery. Located in one of the poorest areas of the state of MP, the village suffered from a variety of problems associated with scarcity of drinking water, lack of Anganwadi Centre’s and absence of employment.

Faced with this situation, we decided to change our strategy by first helping the community to address some of these more urgent problems. Our first step was to file applications with the block administration demanding the provision of these basic services. To our surprise and relief, the demands were addressed; a new Anganwadi centre was established, water problems were resolved and new works were opened up under Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA).

These efforts won us the support of the community who were now convinced of our intentions and were willing to work with us on developing a plan for addressing school needs. Adequate infrastructure facilities was the first need identified by parent. The teaching area in the school consisted of two classrooms and a veranda. The state of the classroom was especially deplorable, as the floors were riddled with potholes. The school also lacked basic drinking water facilities.

To address these problems members of the Village Education Committee (VEC) developed a Plan for repairing the classroom floors and constructing drinking water facilities. To fund both activities it was decided that funds from the previous year’s school maintenance grant, which had not been used, would be combined with this year’s grant. Both activities were slotted to start in September, which was also the period just after the rains when it would be possible to construct water harvesting facilities as well as initiate repair work of classrooms. To complete these activities the community members volunteered to donate their labour.

Thus all plans were made to start work in September. However, there were delays in the transfer of grants and by September the school had yet to receive their funds. When the block level officials were asked about the delay in the transfer of funds, they replied that funds would be transferred soon. The transfers, however, did not take place till January and the Plan which had been made with so much effort was never implemented.

Through this exercise we learnt a number of lessons. The most important however was the lesson that school level planning is a complex process, which involves both the participation and the support of the community and the administration. Thus in mobilizing the community it is important to keep the institutional environment in mind and to ensure that funds arrive on time.

Strengthening School Management Committees

Picking up on Swapna’s analysis is Ram Ratan Jat, PAISA associate, Udaipur District draws a roadmap for strengthening SMC participation.

In the course of my work with the PAISA project I have found that School Management Commitees (SMC) have only been formed on paper. The level of interest taken both by the administration and the community continues to be low. The problem is rooted in the way the administration and the community view the role of the SMC. Administrative officials and Head Masters treat the SMC as a body that they are forced to engage with under the Right To Education (RTE). They do not understand the value of the SMC. Community members, as well, do not consider it important to forgo their earnings and other household responsibilities for participating in SMC meetings.

In this scenario, it is very important to explain to community members and officials the purpose, and importance of participating in and engaging with SMCs. In doing so, one of the most important responsibilities to emphasize is the role of the SMC in managing and monitoring school finances and expenses. It is necessary to highlight that the money that reaches schools is essentially public money. Every person in one way or another pays taxes to the government which is collected and used to fund various government programmes including education.

In my opinion then, it is important to ensure that the community and the school level administration work together to strengthen the role of the SMC. This can be done by;

1) Involving the SMC and the school administration in making of the school plan,

2) Encouraging the SMC to monitor children’s learning levels

3) Emphasizing the role of the SMC in monitoring teacher’s attendance.

1. Authors are PAISA Associates, Accountability Initiative, CPR