Urbanisation in India: What is Municipal Financing?

23 January 2023

According to Census population projections (2020), India’s urban population is estimated to stand at approximately 59 crores in 2035, second only to China. According to Oxford Economics, the top 10 fastest-growing cities in the world over the next two decades will be in this country. With urban spaces rapidly growing and attracting more people and businesses, there is a need for effective governance mechanisms to accommodate and provide for citizens’ needs. Strengthening the financial capabilities of Urban Local Bodies can help achieve this goal.

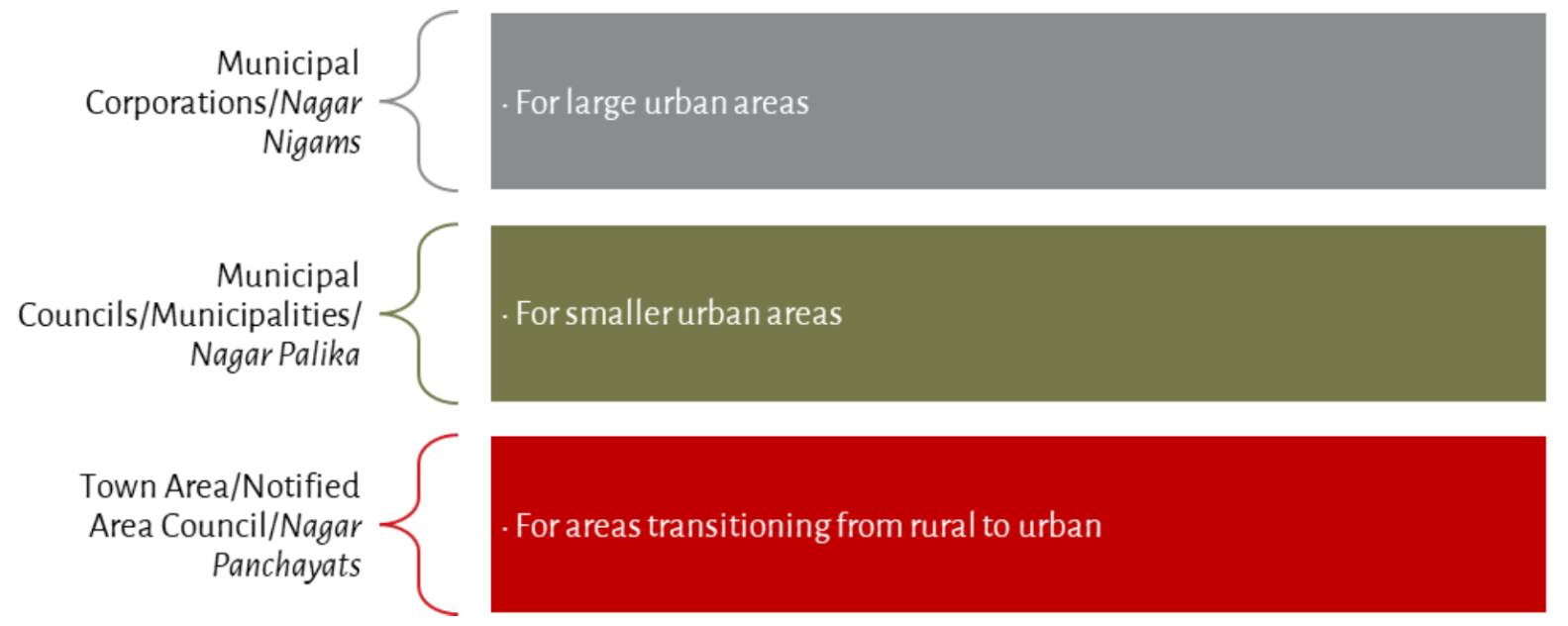

To make governance more accessible, the 74th Amendment to the Constitution formalised the third-tier of government in urban areas. It also identified enormous responsibilities for these Urban Local Bodies (ULBs). According to the census definition, a habitation is declared urban (excluding a municipality, corporation, cantonment board and a notified town area committee) if it has a minimum population of 5,000 people; at least 75 per cent of the male working population is engaged in non-agricultural pursuits; and the population density is at least 400 people per sq km. However, a census town does not have a ULB, changes in governance occur only when a statute is released by the State government.

Figure 1: Types of Urban Local Bodies

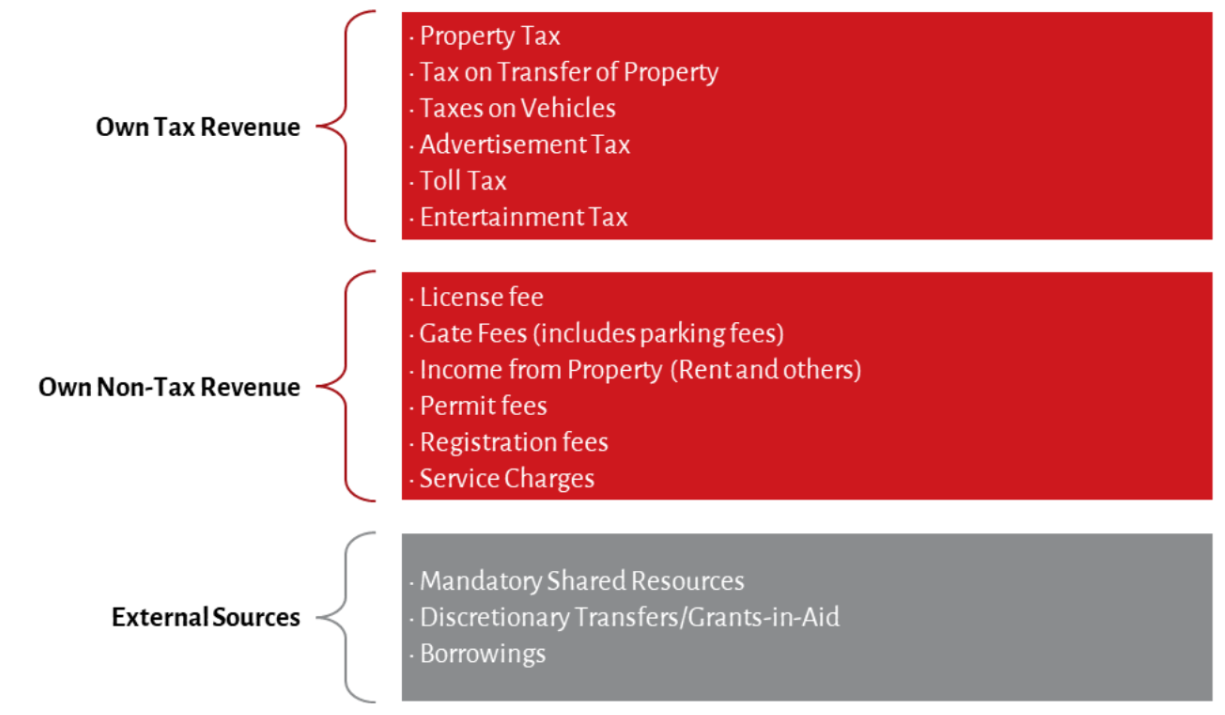

Funding Sources

Substantial funding sources are crucial for the provision of quality service delivery and maintaining effective decentralised governance.

ULBs also have access to own source revenue and the funding received from external sources. Their own sources comprise tax and non-tax revenues of the government. Under the Municipal Act, local bodies are allowed to levy around 25 taxes; only a handful of these taxes are imposed and collected by different ULBs. Property tax among the taxable sources and user charges and parking fees among the non-tax sources make up a major chunk of the own source revenue of the ULBs.

ULBs though heavily depend on external sources of revenue for fulfilling their financing needs. External sources of revenue for the ULBs include:

• Mandatory shared resources which are based on the recommendations from the State Finance Commissions;

• Discretionary Transfers/Grants-in-Aid are Intergovernmental Fiscal Transfers from higher tiers based on needs/policies;

• Borrowings include subsidised loans from higher tiers and these loans can be taken out against bonds as well.

Figure 2: Funding Sources of Urban Local Bodies

In terms of fiscal autonomy, Indian ULBs are one of the weakest local governments internationally. The State exercises elaborate controls on the authority of ULBs to levy taxes, set of rates, grant exemptions, borrow design, and even on the quantum and timing of intergovernmental transfers. (RBI, 2022) The excessive reliance on grants from the Union and state governments coupled with the inability to autonomously access funds have adversely affected ULBs’ ability to function properly. Further, non-financial aspects such as fragmentation of responsibilities between ULBs and other parastatal bodies, inadequate staff strength and skills, low participation of voters in municipal elections, make the situation harder.

There is another phenomenon that indicates how weak ULBs actually are. When a rural area is declared as a ‘census town’, there is resistance from the rural local governments to “go urban” because local politicians fear they would not have access to large amounts of funds for rural development schemes (ICRIER, 2019).

Indian cities continue to face a huge mismatch between their growing responsibilities and deteriorating financial capacity. Our next blog looks at some unconventional sources of funding that ULBs can utilize to close the aforementioned deficit.

Madhur Sharma and Anwesha Mallick are Research Associates at Accountability Initiative.

Read the next blog in the series: Understanding Urban Local Body Financing through Municipal Bonds

Recommended for you

We tried to come up with a clear…

The bureaucracy is considered to be the steel…

Policy Buzz

Keep up-to-date with all that is happening in…

Understanding India’s Health Budgets

The budget is a vital tool to support…

The Mission Creep Problem In Panchayat Finances

First published on Seminar (web-edition), available here. Despite…