The 15th Finance Commission and Changes in the Devolution Formula: Which States Stand to Lose?

4 May 2021

The previous blog explored the overall compositional change in the aggregate transfers to states. The 15th Finance Commission has tried to finely balance two competing objectives – provide adequate resources to states, as well as take a pragmatic approach toward India’s economic recovery following the COVID-19 pandemic.

Nevertheless, states lost out on both the size of the divisible pool as a percentage of GDP (due to lower generation of revenues as well as a higher proportion of cesses and surcharges levied [1]). The fiscal autonomy of resources (due to higher proportions of conditional transfers) was also weakened.

In this blog, we examine the devolution formula that the 15th Finance Commission has proposed,and look at the possible implications for states as a result of these changes.

The devolution of resources to states is not discretionary to the Union government. It is based on a formulaic transfer of resources to states, determined by the Finance Commission. The tax devolution formula is based on the principles of need, equity, and efficiency. In other words, the formula is progressive – states in need of higher assistance receive a larger share of funds devolved.

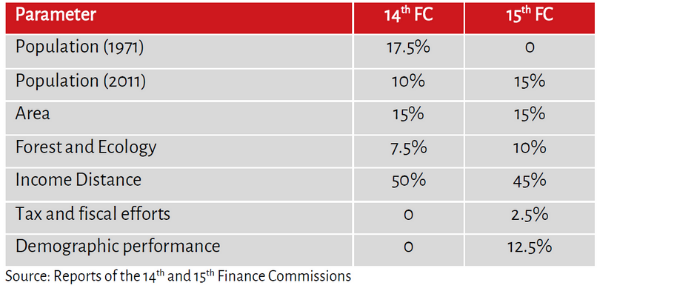

This devolution formula is based on certain indicators. The Finance Commission, after several rounds of deliberations with states, ministries, local bodies, and the civil society, selects the parameters that are most representative of state needs [2]. They also assign appropriate weights to each of these parameters, keeping the core principles of devolution intact.

The 15th Finance Commission made some changes to the parameters that have been used for the devolution formula. There are three changes of note:

1. The use of the 2011 population metric

After members of a Finance Commission are appointed, the Union government sends them a Terms of Reference (TOR).

The TOR of the 15th Finance Commission [3] had earlier created a furore among states [Terms of Reference (15th FC), 2017]. This was due to the Union government directing the then newly formed Commission to use Census 2011 as the metric for population, as opposed to the dated 1971 metric that the previous Commissions had been using [4].

The use of population has long been approved by the Union and states as a simple and effective metric for capturing inequality and inter se challenges for the provision of public services. The higher the population in a state, the more the state government would have to pay to provide for basic services to all its residents. The 7th Finance Commission was the first to use the 1971 population metric and it has been used by all subsequent Commissions as part of the formulaic determination of resource entitlements for different states from the divisible pool [5].

The debate around the use of the 2011 metric instead of the 1971 metric had been ongoing for some time. The 14th Finance Commission had, in its report, mentioned that the use of the 1971 Census data was “unfair” as it failed to capture new demographic changes in states [6].

The TOR for the 15th Finance Commission clearly advocated the use of the 2011 metric in lieu of the 1971 metric. The Union government argued that the 1971 metric was not representative of the newer population trends across states.

Not only had states witnessed diverging population trends since 1971 in terms of natural growth rates and age structures, but migration due to labour and other factors had also changed the demography within states. These newer changes were much more accurately captured from the more recent Census survey (2011) rather than the one in 1971, the government proposed.

However, several states disagreed. This led to what came to be known as the North-South debate. Southern states such as Karnataka, Andhra Pradesh Telangana, and Kerala claimed that the decision to use 2011 parameters overlooked a crucial policy development of Family Planning that had begun in those states in the 1970s [7]. As a result, southern states, in comparison to their northern counterparts, had managed to temper their population growth much more rapidly during the 1970-2010 period.

Thus, according to these states, using the 2011 parameter as one of the factors to determine state share within the divisible pool would mean an advantage for the northern states with larger populations. The southern states, therefore, claimed that their successful policy implementation, including that of family planning campaigns, was effectively being penalised.

2. The demographic performance

The 15th Finance Commission navigated this challenge with the introduction of a balancing parameter in the devolution formula.

Even though the Commission accepted the TOR and used the 2011 population statistic, they introduced ‘demographic performance’ as a parameter, which is basically a proxy for population control. It was introduced to balance the use of the 2011 population metric and reward states that had been effectively curbing population growth since the 1970s.

Table 1: Corresponding weights of parameters selected to determine the vertical devolution

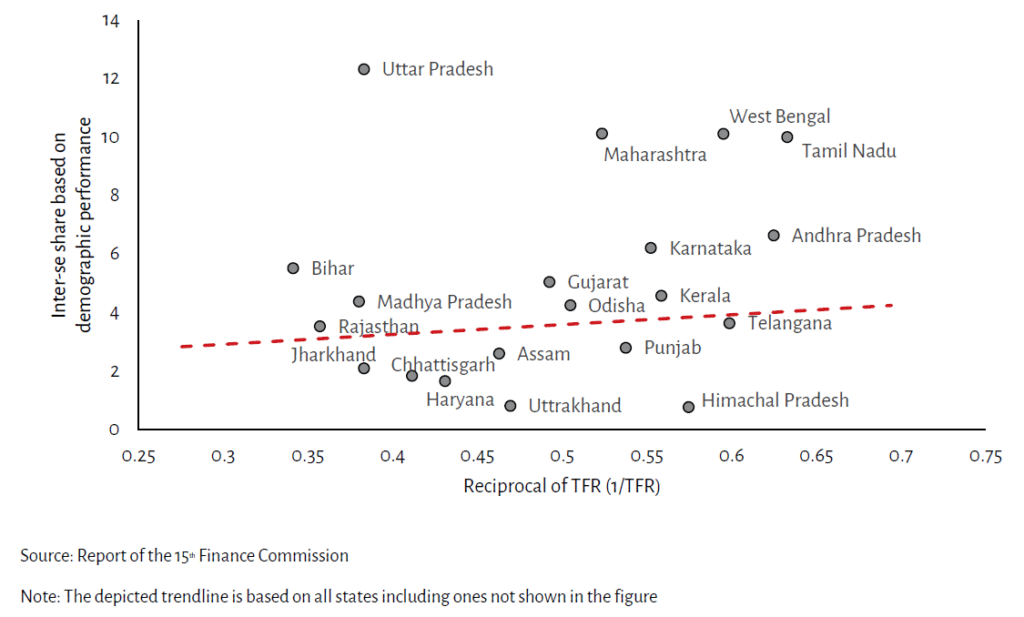

So, did the demographic performance parameter help Southern states? Let us take a look at its finer details.

The demographic performance is measured with the help of a statistic known as ‘total fertility rate’. Total fertility rate (TFR) is the average number of children born to a fertile woman through her/their child-bearing years. The inverse of the TFR has been used by the 15th Finance Commission to calculate the demographic performance. For example, if the typical child-bearing woman has two children in Gujarat, the TFR of Gujarat will be 0.5.

Conceptually, the lower the TFR of a state (or lower the average number of children born to a woman), the higher should be its share of the 12.5 per cent of the divisible pool (the overall weight assigned) that is determined by this parameter (refer to Table 1).

However, as per the Commission’s methodology, the simple inverse of TFR does not only determine an individual state’s share. In order to determine the state-wise share, the inverse of the TFR has been multiplied by the 1971 population to determine the share of each state under the demographic performance parameter. Plotting the inverse of the TFR against the demographic performance parameter shows a weak positive correlation (refer Graph 1).

States that have a higher value on the X-axis (reciprocal of TFR), are the ones with lesser number of children per adult woman. These states are arranged towards the right of the X-axis. The states with a higher value on the Y-axis are the ones that have performed well under the demographic performance parameter as per the current devolution formula.

In other words, these states are receiving a larger share of funds because of their higher score as per demographic performance parameter.

If X (reciprocal of TFR) and Y (demographic performance) were strongly positively correlated, it would indicate that states which had been successful in controlling population are also the ones scoring very high on this parameter and, therefore, eligible for a larger share of funds.

However, the graph depicts a weak positive correlation as can be observed from the trend line.

Graph 1: Correlation between inter se shares based on the demographic performance of states and the reciprocal of TFR

States such as Uttar Pradesh and Bihar rank very high as per the demographic performance factor. This is because they are aided by their comparatively larger population in 1971 despite high TFRs.

States such as Maharashtra, Tamil Nadu, Andhra Pradesh, and West Bengal are some of the bigger states with lower TFRs. These states also gained because of a combination of higher 1971 population and low TFRs.

On the other hand, states with comparatively low TFRs like Telangana and Himachal Pradesh did not gain as much because of relatively lower population shares in 1971.

If the demographic performance was based only on the inverse of TFR and not multiplied by the 1971 population, it would have aided all states that were able to control their population. Some critics have pointed out how the multiplication by the population factor considerably distorts the calculation (Bhattacharjee, 2021) (Hazarika, 2020).

3. The Tax Effort

A similar criticism is also levelled at the usage of the parameter called the ‘Tax Effort’. Tax Effort was previously used by the 11th and 12th finance commissions. The 15th Finance Commission computed the Tax Effort by multiplying the 2011 population with the Own Tax Revenue (OTR) [8] to GSDP (Gross State Domestic Product) ratio, unlike the previous commissions where they used only OTR-GSDP ratio as a criteria to compute the share between states.

Several states suffered a cut in inter se share in the Commission’s method, compared to the conventional method of Tax Effort used by the previous commissions. States such as Gujarat, Tamil Nadu, Maharashtra, Rajasthan, Madhya Pradesh, West Bengal, and Uttar Pradesh with higher population gained in their share under the new method.

States such as Andhra Pradesh, Telangana, Kerala, Haryana, Odisha, Sikkim, Uttarakhand, Himachal Pradesh, Punjab, Jharkhand, and all the North-East states are the states that have suffered a loss.

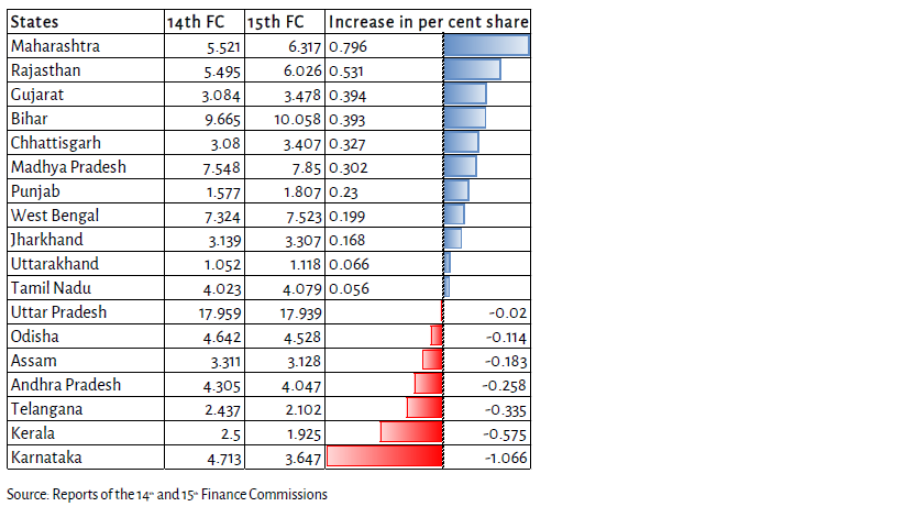

Changes in inter se state share of tax devolution from the 14th Finance Commission to 15th Finance Commission

Overall, the total tax devolution has undergone some changes in formula on which these transfers are based. These changes have had an effect on the aggregate tax devolution to individual states. The inter se tax shares have increased for some states while it has decreased for others.

Maharashtra, Rajasthan, Gujarat, and Bihar are the top four states that have witnessed an increase in their individual shares as a percentage of the total tax devolution.

Maharashtra’s share has increased from 5.52 per cent under the 14th Finance Commission award period to 6.32 per cent under the 15th Finance Commission award period, a total increase of close to 0.8 percentage points. Rajasthan has seen its share go up by 0.53 percentage points, and Gujarat’s share has gone up by 0.39 percentage points over the same period.

Among the states that witnessed a decline in percentage shares include Andhra Pradesh (-0.26 percentage points), Telangana (-0.34 percentage points), and Kerala (-0.58 percentage points). Karnataka witnessed a loss of an entire percentage point from 4.71 per cent to 3.65 per cent. Uttar Pradesh also lost out marginally by 0.02 per cent.

This indicates that the decline cannot be solely explained by the usage of the Census 2011 as the official population parameter, even though the North-South debate has not been satisfactorily addressed by these changes.

Table 2: Inter se state shares from overall tax devolution

The 15th Finance Commission has provided a comprehensive report on state finance estimations and useful recommendations for augmenting state resources under challenging circumstances. However, some questions regarding fiscal autonomy still persist.

Factors such as the changes to the devolution formula, the higher proportion of conditional grants, the higher share of cesses and surcharges, and the conservative limit set on state borrowings have potentially deepened the constraints on state finances which could strain fiscal relations between the Union government and the states.

The next blog will take a detailed look at the 15th Finance Commission’s recommendations for grants-in-aid (specifically Centrally Sponsored Schemes) provided by the Union government.

Meghna is a Research Associate at Accountability Initiative. Vastav is a former Research Associate at Accountability Initiative.

[1] Cesses and surcharges are kinds of taxes that directly accrue to the Union Government and are not shared with states.

[2] List of studies conducted for the 15th FC: https://fincomindia.nic.in/ShowContentOne.aspx?id=27&Section=1

[3] https://fincomindia.nic.in/ShowPDFContent.aspx

[4] The 14th Finance Commission had used both the 1971 and 2011 parameters for formulating the devolution to states. However, this was the first time that an FC was directed to completely abandon the use of the 1971 parameter.

[5] The divisible pool is that portion of gross tax revenue which is distributed between the Centre and the states. The divisible pool consists of all taxes, except surcharges and cesses levied for specific purpose, net of collection charges.

[6] https://fincomindia.nic.in/writereaddata/html_en_files/oldcommission_html/fincom14/others/14thFCReport.pdf

[7] https://iussp.org/sites/default/files/event_call_for_papers/IUSSP_40FP_0.pdf

[8] Own tax revenues are taxes that are levied by the state government and accrue solely to states. Own tax revenue includes (i) receipts from the state excise duty, (iii) entry tax on goods and passengers, and (iii) stamp duty, among others.

References

Bhattacharjee, G. (2021, February 17). The Statesman. Retrieved from The Statesman: https://www.thestatesman.com/opinion/fiscal-roadmap-1502952697.html

Hazarika, D. (2020). Fiscal Architecture OfIndia: A Review On 15th Finance Commission With A Comparison To 14thFinance Commission. European Journal of Molecular & Clinical Medicine. Retrieved from https://ejmcm.com/pdf_7330_c772ef63725e60c5f033b54280fbc47d.html

Terms of Reference (15th FC). (2017). Retrieved from https://fincomindia.nic.in/ShowPDFContent.aspx

One thought on “The 15th Finance Commission and Changes in the Devolution Formula: Which States Stand to Lose?”

Add new comment

Recommended for you

We tried to come up with a clear…

The bureaucracy is considered to be the steel…

Policy Buzz

Keep up-to-date with all that is happening in…

Understanding India’s Health Budgets

The budget is a vital tool to support…

Smart Cities Mission

Smart Cities Mission (SCM) is Government of India’s…

Very good suggestions, I just added this to my RSS feed. What would you suggest in regards to your post that you made a few days ago?

https://kyakarehindimei.com/5-ways-to-make-money-online/